Metro Areas With Largest Percent Gain in Existing Single-Family Home Home Price in 2024 Q2

Download (PNG: 173 KB) | Metro Area Prices & Affordability Data | News Release " data-src="https://www.nar.realtor/sites/default/files/styles/inline_paragraph_image/public/downloadable/2024-q2-10-metro-areas-with-largest-percent-gain-in-existing-home-price-us-map-infographic-08-13-2024-1000w-1500h_0

Read MoreNearly 90% of Metro Areas Registered Home Price Gains in Second Quarter of 2024

Key Highlights Single-family existing-home sales prices rose in 89% of measured metro areas – 199 of 223 – in the second quarter, down from 93% in the previous quarter. The national median single-family existing-home price rose 4.9% from a year ago to $422,100. Twenty-nine markets (13%) experienced

Read More-

On this International Cat Day, we celebrate pet owners. Did you know there are more households with pets than children? These beloved pets are a driver of a major facet of economic activity: home buying. About one-fifth of recent home buyers considered their pet in their neighborhood choice—a share

Read More Instant Reaction: Mortgage Rates, August 8, 2024

Facts: The 30-year fixed mortgage rate from Freddie Mac dropped to 6.47% this week, compared to 6.73% last week. At 6.47%, with 20% down, a monthly mortgage payment on a home with a price of $400,000 is $2,016. Compared to October 2023, when rates were 7.79%, this is a monthly payment difference of

Read MoreJuly 2024 Commercial Real Estate Market Insights

" data-src="https://cdn.nar.realtor/sites/default/files/styles/wysiwyg_small2/public/2024-07-commercial-real-estate-market-insights-08-07-2024-300w-433h.png?itok=e3UVY_e0" class="b-lazy" width="200" height="289" alt="Cover of the July 2024 Commercial Real Estate Market Insights report" title="Cover

Read MoreUnlocking Global Opportunities

On July 31, 2024, NAR held a virtual webinar that provided findings from the 2024 International Transactions in U.S. Residential Real Estate report, and discussed how REALTORS® are unlocking global opportunities in the residential real estate market. The speakers were Stephanie Aker, manager of NAR

Read MoreInstant Reaction: Jobs, August 2, 2024

Mortgage rates are plunging on the news of weak job growth and rising unemployment. The 4.3% unemployment rate is the highest since coming out of the COVID lockdown and higher than the 3.5% unemployment rate right before the COVID-19 arrival. The hourly wage gain of 3.2% is the weakest in 3 years. T

Read MoreContract Signings Rise as More Listings Hit the Market

" data-src="https://cdn.nar.realtor/sites/default/files/styles/inline_paragraph_image/public/gettyimages-1166187606.jpg?itok=sHTn3o8s" class="b-lazy" width="1200" height="580" alt="Real estate agent shaking hands with clients inside home"> © monkeybusinessimages - iStock/Getty Images Plus Home buyer

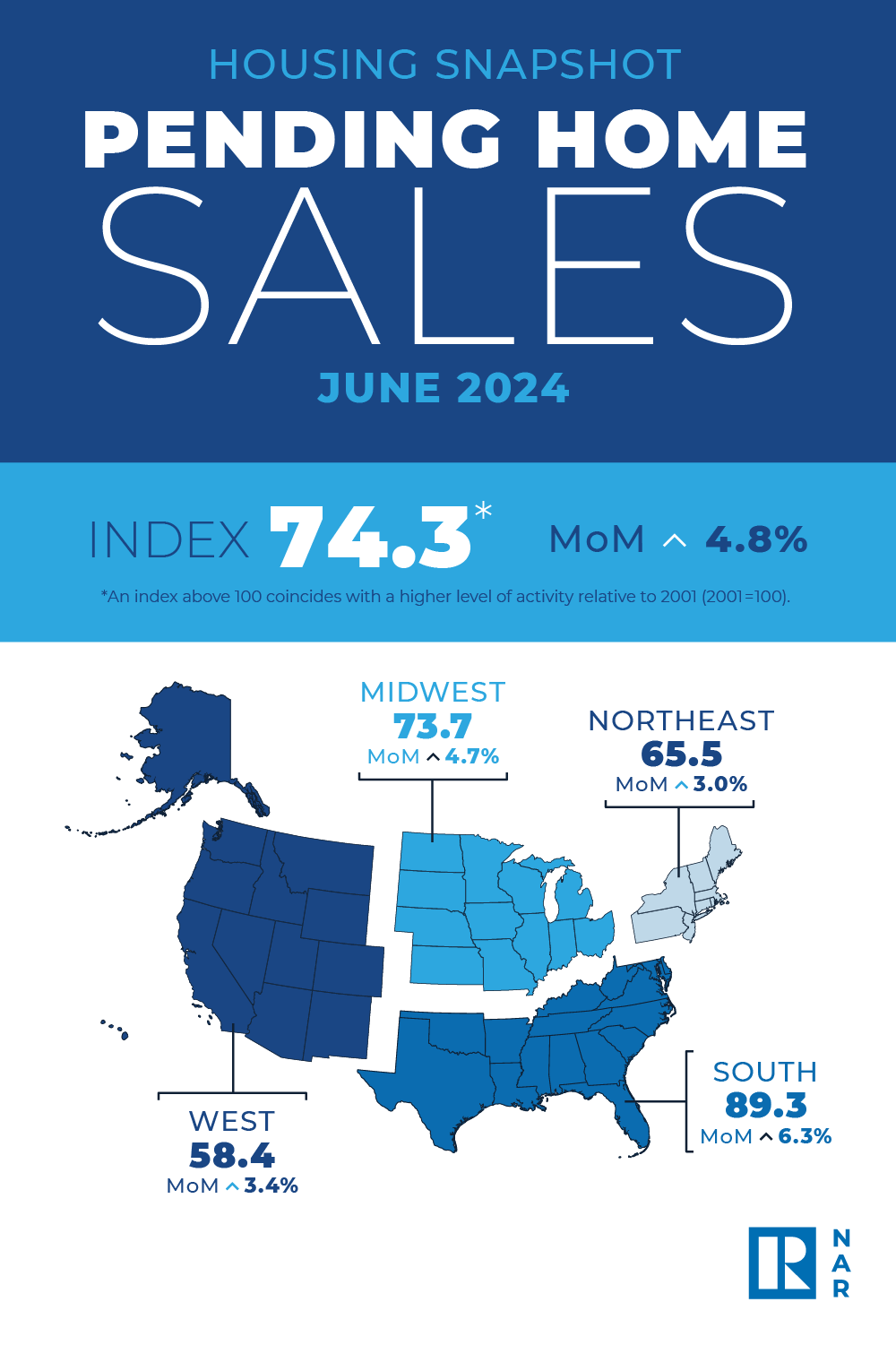

Read MorePending Home Sales Rose 4.8% in June

Key Highlights Pending home sales intensified 4.8% in June. Month over month, contract signings increased in all four U.S. regions. Compared to one year ago, pending home sales declined in the Northeast, Midwest and South, but improved in the West. " data-src="https://www.nar.realtor/sites/default/f

Read MoreInstant Reaction: Mortgage Rates, July 25, 2024

Facts: The 30-year fixed mortgage rate from Freddie Mac was nearly unchanged at 6.78% this week vs 6.77% last week. At 6.78%, with 20% down, a monthly mortgage payment on the median priced existing home of $426,900 is $2,222; with 10% down, it is $2,500. Positive: Also out today: GDP was stronger th

Read More-

According to NAR's Housing Affordability Index, housing affordability declined nationally in May compared to the previous month. The monthly mortgage payment increased by 3.9%, while the median price of single-family homes rose by 5.7% (from $401,500 to $424,500) year-over-year. The monthly mortgage

Read More -

" data-src="https://cdn.nar.realtor/sites/default/files/styles/wysiwyg_small2/public/2024-06-foot-traffic-sentrilock-home-showings-report-cover-07-23-2024-300w-400h.png?itok=zilgSYnu" class="b-lazy" width="200" height="267" alt="Cover of the June 2024 Foot Traffic NAR Sentrilock Home Showings report

Read More July 2024 NAR Real Estate Forecast Summit: Residential Update

On July 22, 2024, from 12:00 – 1:00 p.m. ET, NAR held a virtual economic and real estate summit that provided an outlook on the changing residential real estate market. The speakers were NAR Chief Economist Lawrence Yun and NAR Deputy Chief Economist Jessica Lautz. " data-src="https://cdn.nar.realto

Read MoreExisting-Home Sales Slipped 5.4% in June; Median Sales Price Jumps to Record High of $426,900

Key Highlights Existing-home sales faded 5.4% in June to a seasonally adjusted annual rate of 3.89 million. Sales also slumped 5.4% from one year ago. The median existing-home sales price bounced 4.1% from June 2023 to $426,900 – the second straight month it reached an all-time high and the twelfth

Read MoreNAR Real Estate Forecast Summit: Residential Update, July 2024

" data-src="https://cdn.nar.realtor/sites/default/files/styles/wysiwyg_small2/public/nar-real-estate-forecast-summit-jessica-lautz-presentation-slides-cover-07-22-2024-1300w-867h.png?itok=fZAnTo6G" class="b-lazy" width="200" height="133" alt="Cover of Jessica Lautz's presentation slides: NAR Real Es

Read MoreReal Estate and Economic Outlook July 2024

" data-src="https://cdn.nar.realtor/sites/default/files/styles/wysiwyg_small2/public/real-estate-and-economic-outlook-midyear-nar-forecast-summit-lawrence-yun-presentation-slides-cover-07-22-2024-1300w-867h.png?itok=iPBJVkx2" class="b-lazy" width="200" height="133" alt="Cover of Lawrence Yun's prese

Read MoreInstant Reaction, Mortgage Rates, July 18, 2024

Facts: The 30-year fixed mortgage rate from Freddie Mac fell further to 6.77% over the last week from 6.89%. At 6.77%, with 20% down, a monthly mortgage payment on a home of $400,000 is $2,080; with 10% down, it is $2,340. Positive: This is the lowest mortgage rate reported since March 14. This is t

Read MoreTransacciones internacionales con bienes raíces residenciales en EE. UU.

" data-src="https://cdn.nar.realtor/sites/default/files/styles/wysiwyg_small2/public/2024-international-transactions-in-us-residential-real-estate-report-spanish-language-version-cover-07-17-2024-300w-375h.png?itok=vrw96aXt" class="b-lazy" width="200" height="250" alt="Portada de las Transacciones i

Read MoreInstant Reaction Housing Starts, July 17, 2024

New apartment units completed reached a 50-year high in June. That is truly a wow. The rents have stopped rising in many cities due to the oversupply of rental units. Rents whether on apartments or on single-family rentals have fallen in Austin, Nashville, Charlotte, and Phoenix where the supply has

Read MoreAnnual Foreign Investment in U.S. Existing Homes Sales Decreased 21.2% to $42 Billion

Key Highlights International buyers purchased $42 billion worth of U.S. residential properties from April 2023 to March 2024, down 21.2% from the prior year. The 54,300 existing homes sold – the lowest since NAR began tracking in 2009 – slid 36% from the previous year. The average ($780,300) and med

Read More

Categories

Recent Posts